Honasa Consumer : The house of brands

Honasa Consumer Private Limited, the parent company of Mamaearth (and other brands), has recently filed for its IPO. In this write-up, we will learn more about the company, the BPC market in India, and valuations (much talked about).

About Honasa

Honasa Consumer was launched in 2016 to solve the customer's need for safe-to-use natural products that are toxin-free and made with natural ingredients. The founders, Ghazal Alagh and Varun Alagh couldn’t find any toxin-free and organic product for their newborn. Feeling that this problem might be faced by lots of consumers, they decided to start Mamaearth with the promise of toxin-free products made with natural ingredients. As of 30th September 2022, Honasa has added five more brands to the portfolio.

The success of the Mamaearth brand has helped them in developing a repeatable brand-building playbook that has helped them in scaling their new brands at a rapid pace. They have an asset-light contract manufacturing model, with 37 contract manufacturers, that gives them the benefit of economies of scale even at small batch sizes and is also flexible to scale up production as needed. They ensure that the contract manufacturers adhere to stringent quality control and that regular checks are conducted to ensure compliance.

The Playbook

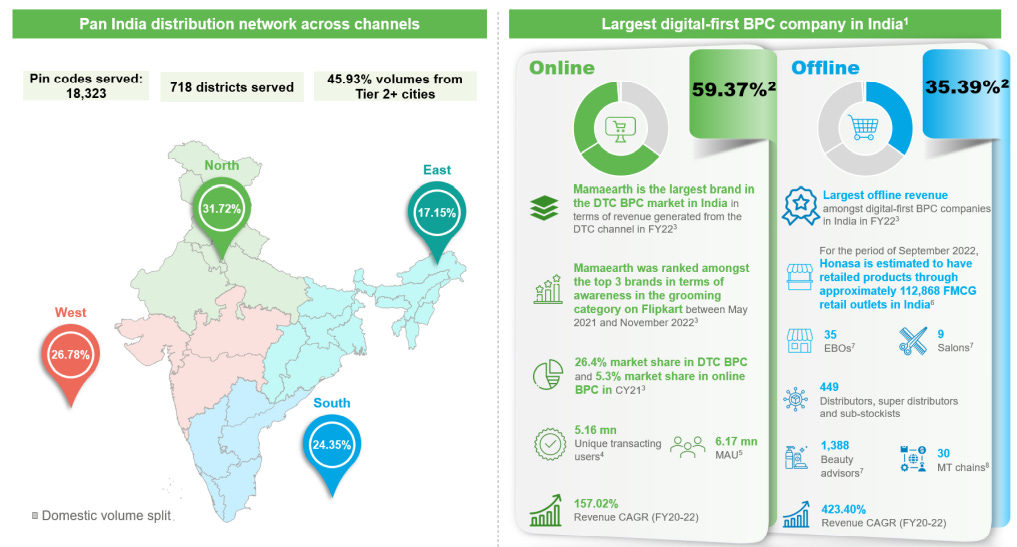

Honasa leverages the online channels to generate trials among early users, engage with consumers directly and test its product-market fit. Once a brand/product reaches a mature stage, it is selectively introduced in offline stores to drive penetration amongst a large consumer base. The digital-first approach helps them to incorporate valuable customer feedback across new product launches. Honasa launched 225 new SKUs (2.6 times the industry median) in the first half of FY23, contributing ~44% to the increase in revenue from operations.

They leverage their data ecosystem to understand consumers across demographics, behavioral, and transactional variables. Millennials are most influenced by other millennials and respond better to content that is meaningful and contextualized to their needs.

Their social listening and tracking platform captures consumer sentiments and identifies emerging trends and propositions (rice water for frizzy hair, green tea for open pores) that help them launch new products. Their competitive intelligence platform for e-commerce tracks market share movements across BPC categories to identify value propositions and price points gaining traction with consumers.

Future Strategies

Honasa plans to continue to invest in brand building (very high advertisement and promotions budget, more on this later) to drive awareness. To support their offline plans, they also plan to focus on television advertising that is completely different from their cohort-based personalized marketing activities. They intend to leverage the offline channel to drive penetration for mainstream BPC categories such as shampoo, hair oil, and face wash.

The company plans to incubate/acquire new brands across new value propositions and price points and leverage its playbook to grow these brands at a rapid pace. They will also open Exclusive Brand Outlets across malls and high-street outlets to create a richer brand experience

With the acquisition of BBlunt, the company plans to expand its presence in the professional salon channel. The channel is expected to provide a ready base of consumers to generate trials

BPC Market in India - Long way to go

The BPC (Beauty and Personal Care) market in India is expected to grow at a CAGR of 12% until 2026 to reach $30 billion, and the online BPC market is expected to grow much faster, with a CAGR of 27% to reach $8.4 billion by 2026. The BPC market in India is significantly underpenetrated. BPC spending per capita in China is 4.5x that of India, and even Bangladesh has a higher per capita amount spent on the BPC category

The share of organized retail in BPC is expected to reach 45-55% by 2026 compared to ~33% in 2021.

Digital-first brands are defined as brands that make at least 60% of their revenue from online channels. The cost of launching and reaching the national scale for a digital brand is much lower than for traditional brands. Digital brands leverage the unlimited shelf space and instant access to actionable data that the online channel provides. Offline is still the biggest channel for BPC products and is more profitable than online channels. However, the growth is being driven by online channels - marketplaces (Amazon, Flipkart, Myntra, Nykaa, etc.) and their own digital platforms (mamaearth.in, thedermaco.com, aqualogica.in, etc.). The marketplace channel is expected to grow at 25%, and their own digital platform channels are expected to grow higher at 45% CAGR by 2026.

Drivers of the BPC market in India

Premiumization: BPC products are classified into three price brands - mass, masstige, and premium. The Masstige segment, which is priced 10-15% higher than the mass products, is the fastest growing price segment and, by 2026, is expected to be the largest segment by value (currently mass price segment is the largest)

Changing category mix: Growth is being led by face care and makeup. There’s an increasing awareness and demand for newer regimes (cleansing, exfoliating, moisturizing, etc.)

Favorable demographics: Consumers in the age group of 25-35 years are the most active BPC buyers, and India has the largest population base of Gen Z and millennials in the world

Increasing contribution from beyond the metros: There has been an increase in aspirational spending on BPC products from non-metros, enabled by rising disposable income, increasing female workforce participation, growing influence of social media, etc. The growth of e-commerce has also enabled access to masstige and premium products in non-metros

Competition

Honasa faces high competition from new-age digital brands and legacy brands with strong distribution. Legacy brands such as HUL and Marico have launched their own D2C extensions (Lakme, Parachute, Saffola) or new brands (Simple, Beardo) to take on the rise of digital-first companies. These launches by legacy players are at comparatively lower prices, which may hurt future prospects of Honasa.

Honasa may not be able to sustain its pricing over the long run, and its gross margins may come down, creating further pressure on profitability. Also, they are deriving ~35% of their revenue from offline channels, where the competition for shelf space is very high.

Numbers

The addressable market for Honasa is expected to be $45-$50 billion by 2026, of which BPC is expected to be $30 billion and $15-$20 billion for salon services

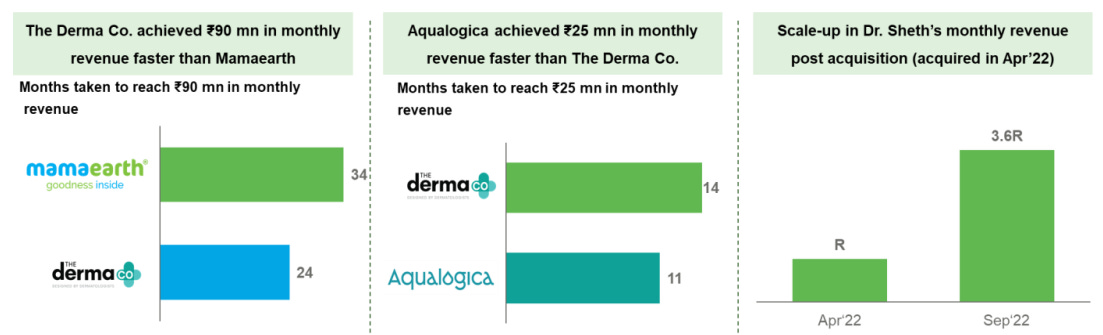

Mamaearth is the fastest growing BPC brand in India to reach an annual turnover of Rs. 1000 crore within 6 years of launch

The revenue growth for the last 3 years has been at a CAGR of ~193%

Going ahead, the revenue growth is projected to be 45-50% until 2026

Valuation

The most talked about topic. According to sources, Honasa is seeking a valuation of ~$3 billion (Rs. 24,000 crores), a 2.5x increase from its last funding round in January 2022. The internet community is valuing them on the basis of the P/E ratio, which is not the correct metric to value such companies. The kind of revenue growth that Honasa is generating needs high reinvestment in brand building. Thus, their advertisement expenses as a percentage of revenue are very high compared to other companies.

If they reduce their advertisement expenses to the level of legacy companies, their profits would be around ~Rs. 450 crores for FY23. An average P/E of 55 would give them a valuation of ~Rs. 24,750 crores. But, we know it’s not possible for them to reduce their advertisement expenses to that level, as they don’t have a great brand recall yet, and this may slow down the revenue growth.

MarketCap/Sales Ratio

At an expected growth rate of 40% CAGR, Honasa is expected to end FY26 with revenue of ~Rs. 4000 crores. With an average multiple of 8 times sales, the valuation at FY26 would be ~Rs. 32000 crores, discounting this at 12% to present, gives a valuation of ~Rs. 24000 crores.

Return on Ad Spends

The valuation looks justified if we ignore their Return on Ad spends. Return on Ad spends measures the additional amount of revenue per rupee spent on advertisement and promotion. Their ROAs have been the same for the last 4 years (~2.5), which implies either they are not able to generate repeat transactions from their existing customers or they are spending too much on customer acquisition for their new brands. The narrative being floated is that they have very few loyal customers who buy only once. We believe they are still building their brand, and things may improve further with time.

Valuations aside, Honasa has been doing the right things to reach this scale. We hope the legacy companies take a note out of their playbook and bring in innovation that helps the industry at large. As for their IPO, we will let the markets decide the price at which people are willing to buy.